On the Constrained Time-Series Generation Problem

{kind=link}

Abstract

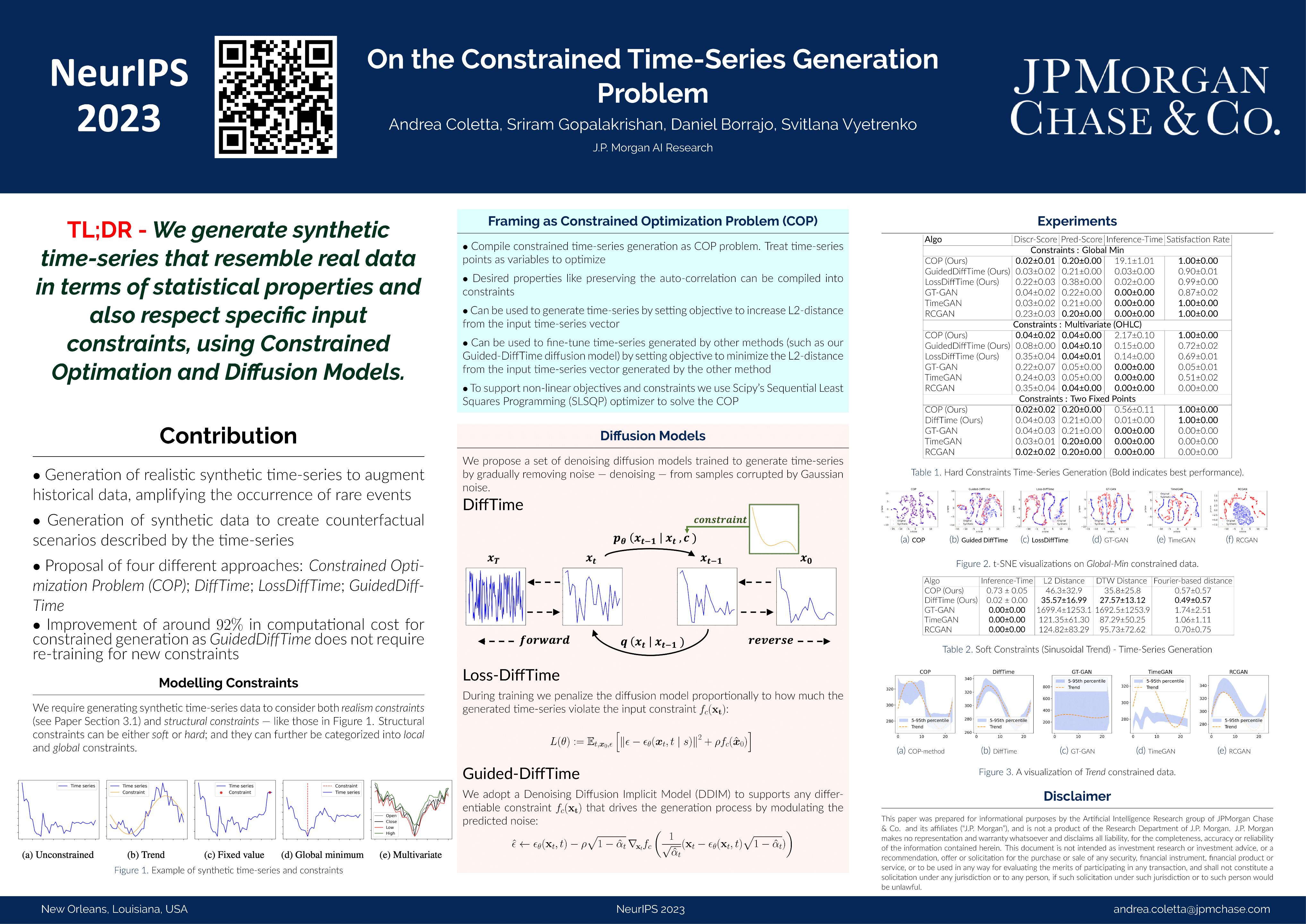

Synthetic time series are often used in practical applications to augment the historical time series dataset, amplify the occurrence of rare events and also create counterfactual scenarios.Distributional-similarity (which we refer to as realism) as well as the satisfaction of certain numerical constraints are common requirements for counterfactual time series generation. For instance, the US Federal Reserve publishes synthetic market stress scenarios given by the constrained time series for financial institutions to assess their performance in hypothetical recessions.Existing approaches for generating constrained time series usually penalize training loss to enforce constraints, and reject non-conforming samples. However, these approaches would require re-training if we change constraints, and rejection sampling can be computationally expensive, or impractical for complex constraints.In this paper, we propose a novel set of methods to tackle the constrained time series generation problem and provide efficient sampling while ensuring the realism of generated time series. In particular, we frame the problem using a constrained optimization framework and then we propose a set of generative methods including 'GuidedDiffTime', a guided diffusion model. We empirically evaluate our work on several datasets for financial and energy data, where incorporating constraints is critical. We show that our approaches outperform existing work both qualitatively and quantitatively, and that 'GuidedDiffTime' does not require re-training for new constraints, resulting in a significant carbon footprint reduction, up to 92% w.r.t. existing deep learning methods.