No-Regret Learning in Dynamic Competition with Reference Effects Under Logit Demand

Mengzi Amy Guo ⋅ Donghao Ying ⋅ Javad Lavaei ⋅ Zuo-Jun Shen

2023 Poster

{kind=link}

Abstract

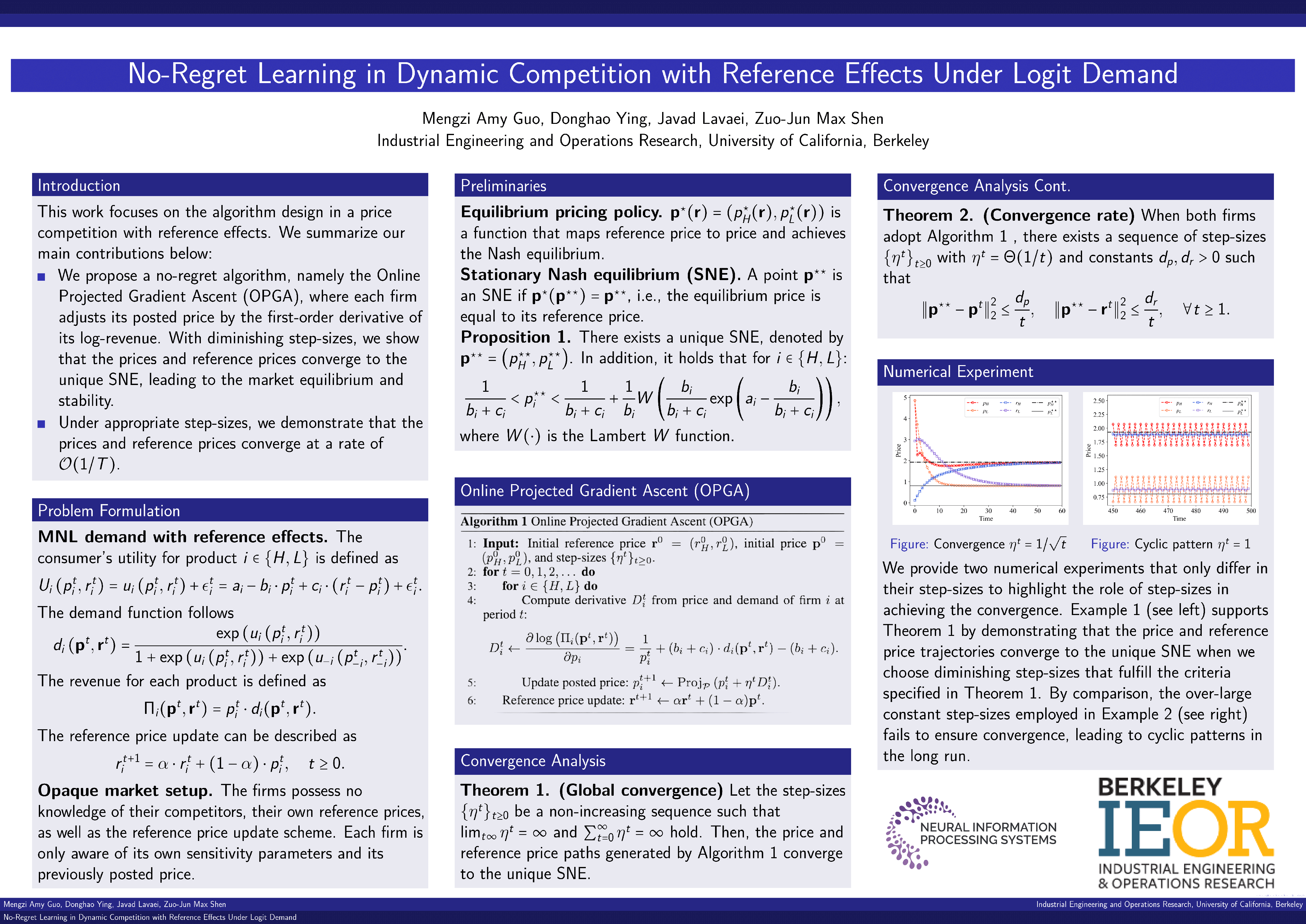

This work is dedicated to the algorithm design in a competitive framework, with the primary goal of learning a stable equilibrium. We consider the dynamic price competition between two firms operating within an opaque marketplace, where each firm lacks information about its competitor. The demand follows the multinomial logit (MNL) choice model, which depends on the consumers' observed price and their reference price, and consecutive periods in the repeated games are connected by reference price updates. We use the notion of stationary Nash equilibrium (SNE), defined as the fixed point of the equilibrium pricing policy for the single-period game, to simultaneously capture the long-run market equilibrium and stability. We propose the online projected gradient ascent algorithm (OPGA), where the firms adjust prices using the first-order derivatives of their log-revenues that can be obtained from the market feedback mechanism. Despite the absence of typical properties required for the convergence of online games, such as strong monotonicity and variational stability, we demonstrate that under diminishing step-sizes, the price and reference price paths generated by OPGA converge to the unique SNE, thereby achieving the no-regret learning and a stable market. Moreover, with appropriate step-sizes, we prove that this convergence exhibits a rate of $\mathcal{O}(1/t)$.

Video

Chat is not available.

Successful Page Load