Adaptive Normalization for Non-stationary Time Series Forecasting: A Temporal Slice Perspective

{kind=link}

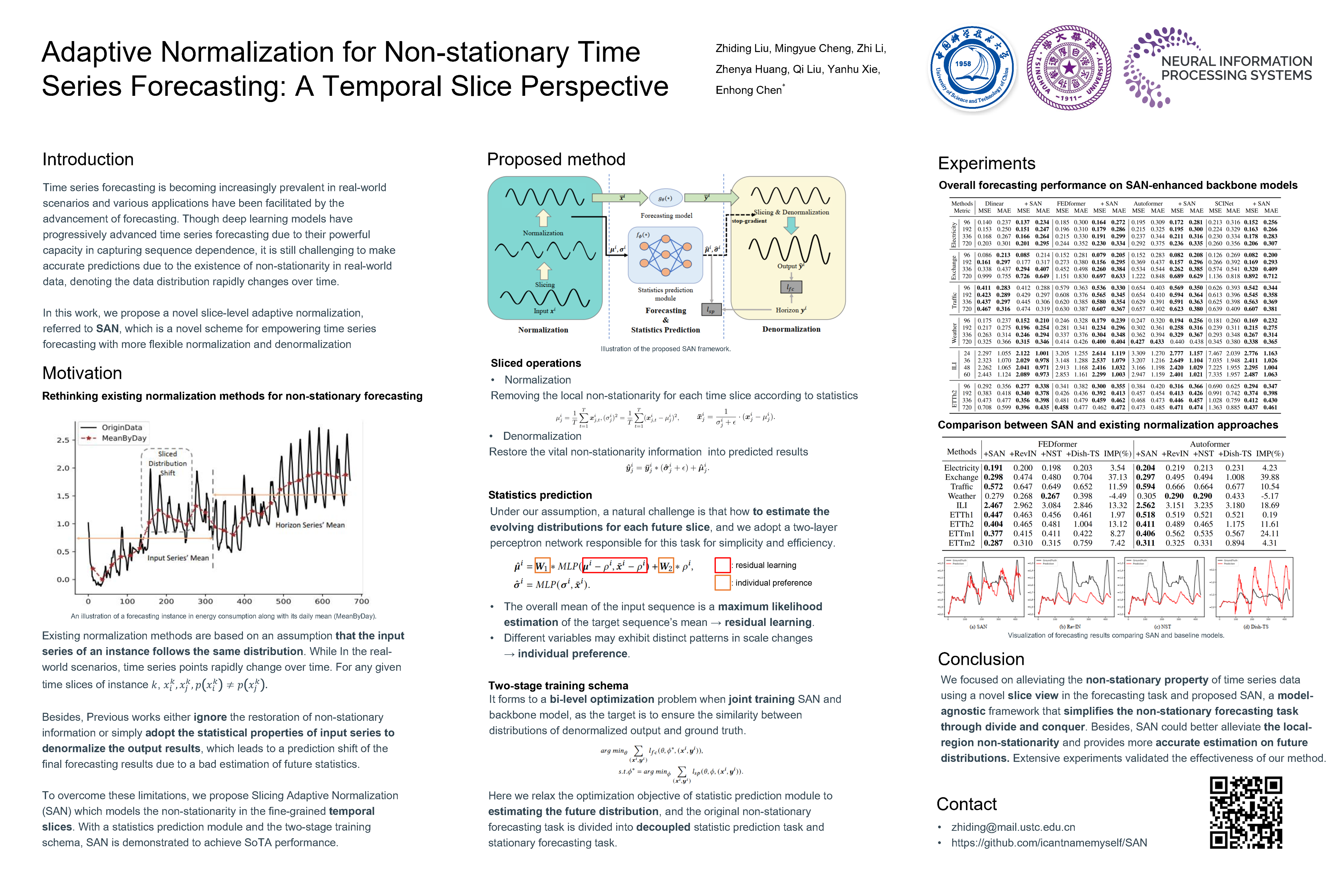

Abstract

Deep learning models have progressively advanced time series forecasting due to their powerful capacity in capturing sequence dependence. Nevertheless, it is still challenging to make accurate predictions due to the existence of non-stationarity in real-world data, denoting the data distribution rapidly changes over time. To mitigate such a dilemma, several efforts have been conducted by reducing the non-stationarity with normalization operation. However, these methods typically overlook the distribution discrepancy between the input series and the horizon series, and assume that all time points within the same instance share the same statistical properties, which is too ideal and may lead to suboptimal relative improvements. To this end, we propose a novel slice-level adaptive normalization, referred to \textbf{SAN}, which is a novel scheme for empowering time series forecasting with more flexible normalization and denormalization. SAN includes two crucial designs. First, SAN tries to eliminate the non-stationarity of time series in units of a local temporal slice (i.e., sub-series) rather than a global instance. Second, SAN employs a slight network module to independently model the evolving trends of statistical properties of raw time series. Consequently, SAN could serve as a general model-agnostic plugin and better alleviate the impact of the non-stationary nature of time series data. We instantiate the proposed SAN on four widely used forecasting models and test their prediction results on benchmark datasets to evaluate its effectiveness. Also, we report some insightful findings to deeply analyze and understand our proposed SAN. We make our codes publicly available.