A Neural Universal Differential Equation (UDE) Approach for Modeling and Forecasting NIFTY 50 Index (Indian Stock Market Index) Prices and Drifts

{kind=link}

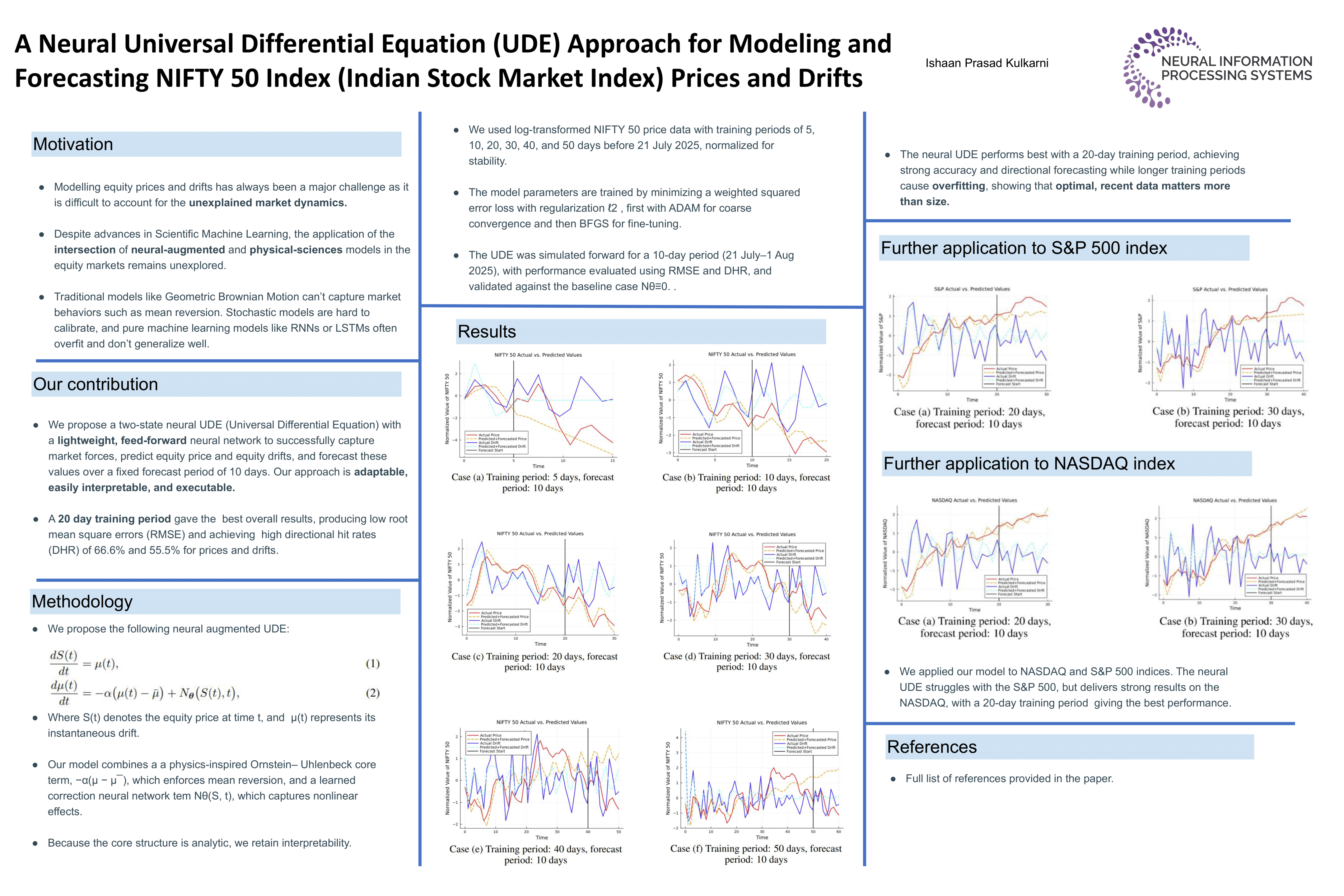

Abstract

Modeling equity prices and equity drifts has been a major challenge, as it requires investors and traders to account for unexplained market dynamics. Despite the rapid progress of Scientific Machine Learning frameworks, the intersection of neural-augmented and physical-science-inspired models remains an unexplored avenue for systematic applications in the equity markets domain. In this study, we propose a two-state neural UDE (Universal Differential Equation) model approach to successfully capture market forces, predict equity price and equity drifts, and forecast these values over a fixed forecast period of 10 days. Through hyperparameter optimization and validation metrics, a 20 day training period gave the best overall results, producing low root mean square errors (RMSE) and achieving high directional hit rates (DHR) of 66.6% and 55.5% for prices and drifts. Our approach is adaptable, easily interpretable, and executable. This study opens a door to investigate applications of Scientific Machine Learning frameworks in forecasting tasks for the equity markets domain.