SOFTS: Efficient Multivariate Time Series Forecasting with Series-Core Fusion

{kind=link}

Abstract

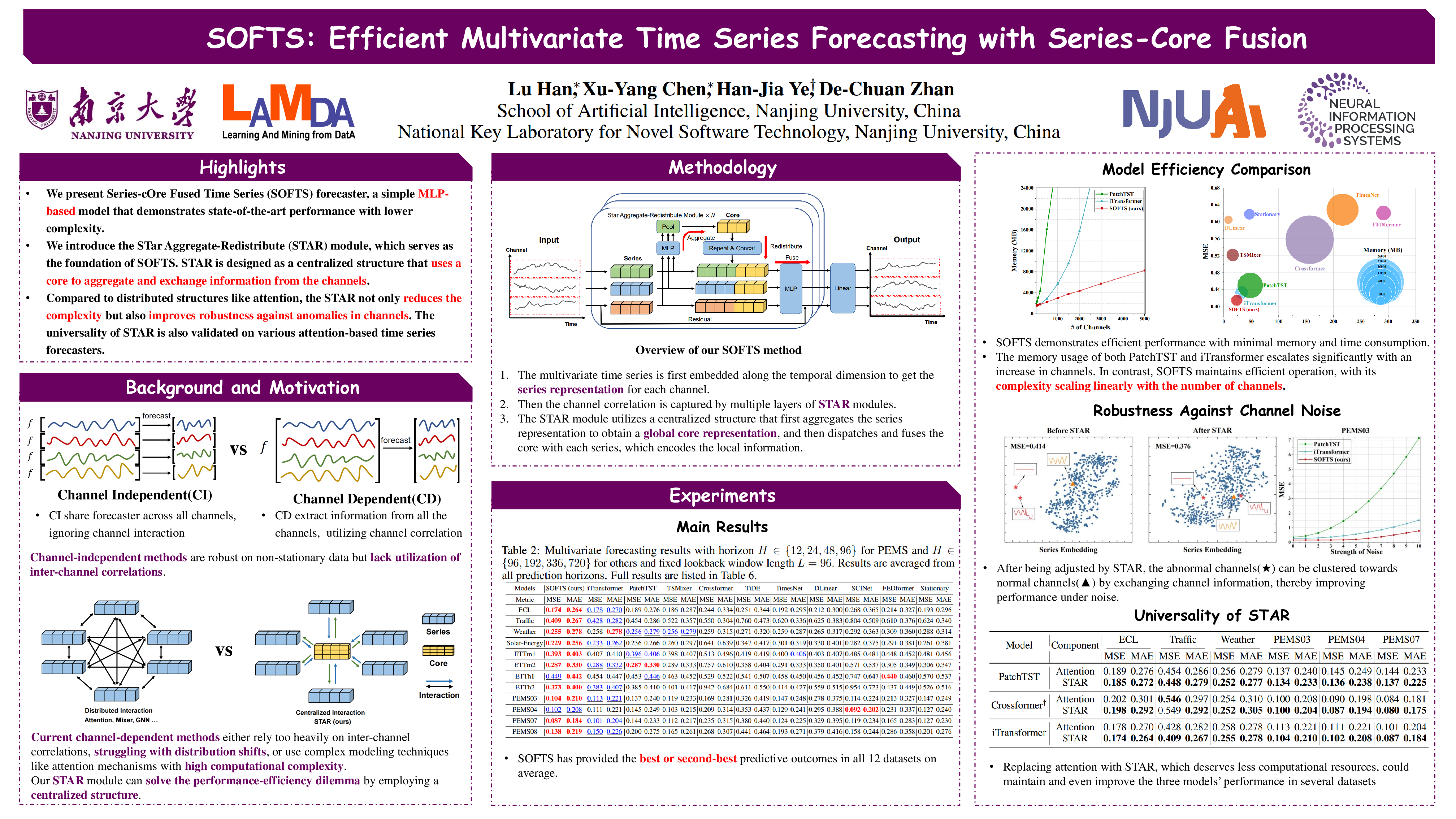

Multivariate time series forecasting plays a crucial role in various fields such as finance, traffic management, energy, and healthcare. Recent studies have highlighted the advantages of channel independence to resist distribution drift but neglect channel correlations, limiting further enhancements. Several methods utilize mechanisms like attention or mixer to address this by capturing channel correlations, but they either introduce excessive complexity or rely too heavily on the correlation to achieve satisfactory results under distribution drifts, particularly with a large number of channels. Addressing this gap, this paper presents an efficient MLP-based model, the Series-cOre Fused Time Series forecaster (SOFTS), which incorporates a novel STar Aggregate-Redistribute (STAR) module. Unlike traditional approaches that manage channel interactions through distributed structures, \textit{e.g.}, attention, STAR employs a centralized strategy to improve efficiency and reduce reliance on the quality of each channel. It aggregates all series to form a global core representation, which is then dispatched and fused with individual series representations to facilitate channel interactions effectively. SOFTS achieves superior performance over existing state-of-the-art methods with only linear complexity. The broad applicability of the STAR module across different forecasting models is also demonstrated empirically. We have made our code publicly available at https://github.com/Secilia-Cxy/SOFTS.