CausalStock: Deep End-to-end Causal Discovery for News-driven Multi-stock Movement Prediction

{kind=link}

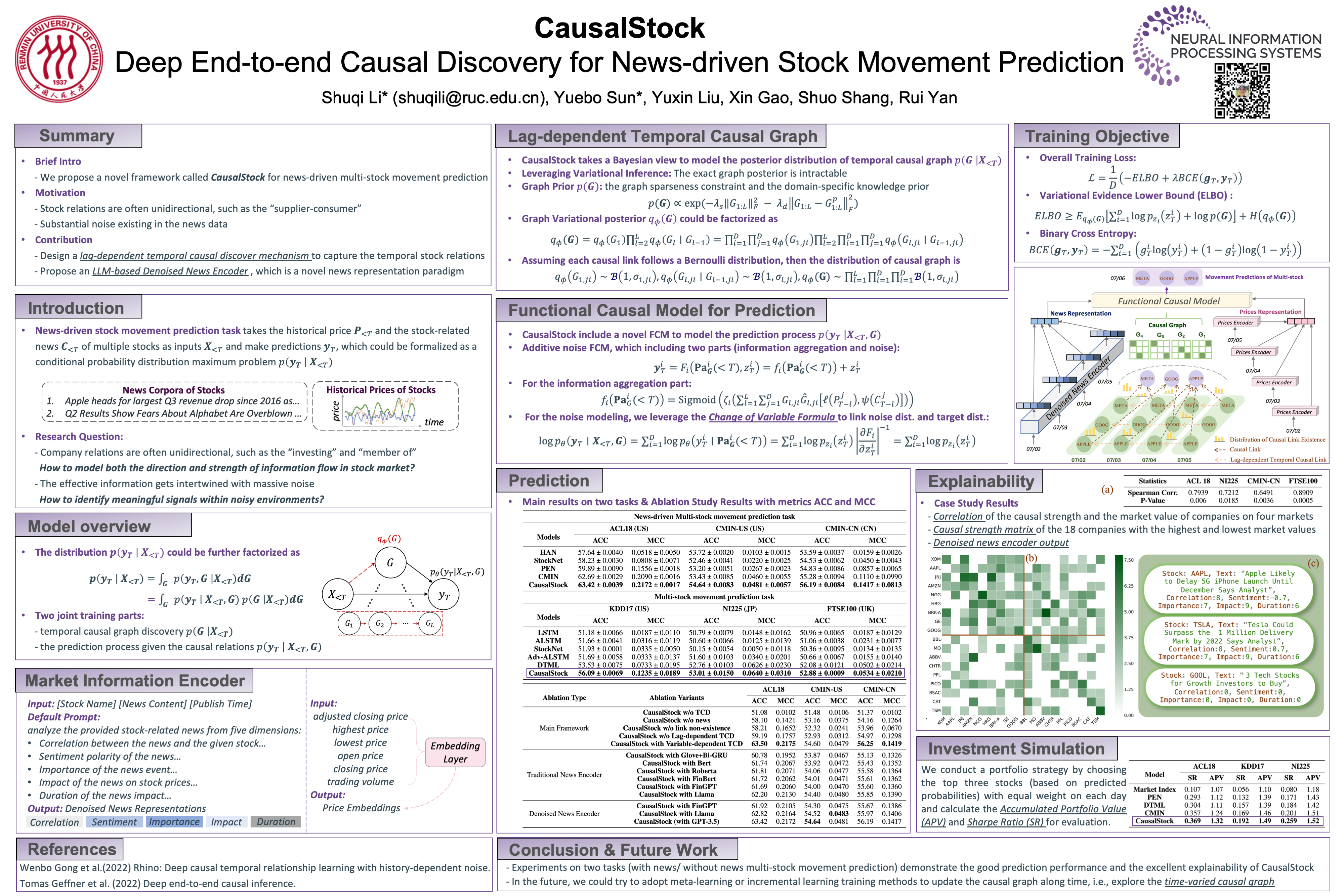

Abstract

There are two issues in news-driven multi-stock movement prediction tasks that are not well solved in the existing works. On the one hand, "relation discovery" is a pivotal part when leveraging the price information of other stocks to achieve accurate stock movement prediction. Given that stock relations are often unidirectional, such as the "supplier-consumer" relationship, causal relations are more appropriate to capture the impact between stocks. On the other hand, there is substantial noise existing in the news data leading to extracting effective information with difficulty. With these two issues in mind, we propose a novel framework called CausalStock for news-driven multi-stock movement prediction, which discovers the temporal causal relations between stocks. We design a lag-dependent temporal causal discovery mechanism to model the temporal causal graph distribution. Then a Functional Causal Model is employed to encapsulate the discovered causal relations and predict the stock movements. Additionally, we propose a Denoised News Encoder by taking advantage of the excellent text evaluation ability of large language models (LLMs) to extract useful information from massive news data. The experiment results show that CausalStock outperforms the strong baselines for both news-driven multi-stock movement prediction and multi-stock movement prediction tasks on six real-world datasets collected from the US, China, Japan, and UK markets. Moreover, getting benefit from the causal relations, CausalStock could offer a clear prediction mechanism with good explainability.