Contextual Dynamic Pricing with Unknown Noise: Explore-then-UCB Strategy and Improved Regrets

Yiyun Luo ⋅ Will Wei Sun ⋅ Yufeng Liu

2022 Poster

{kind=link}

Abstract

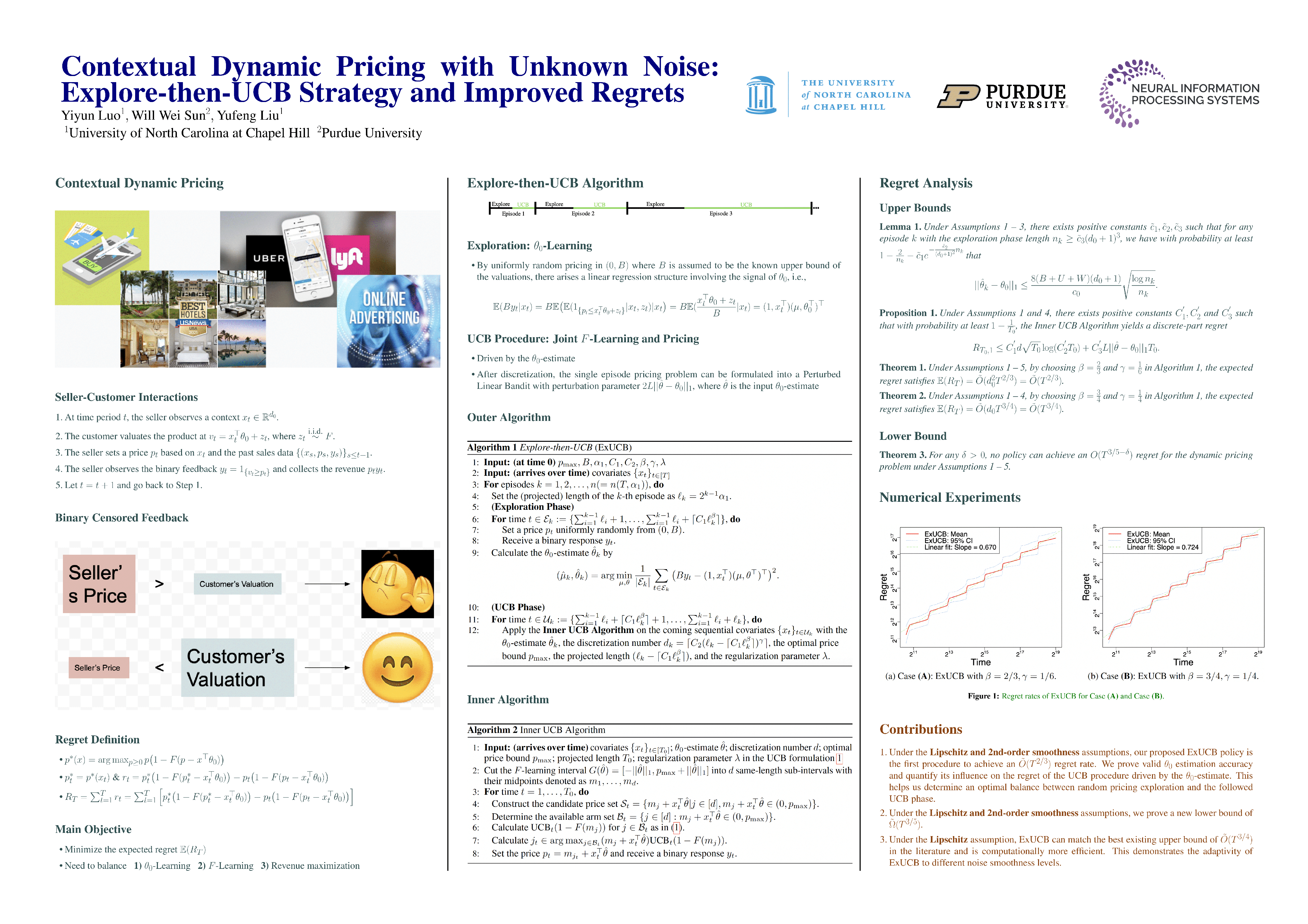

Dynamic pricing is a fast-moving research area in machine learning and operations management. A lot of work has been done for this problem with known noise. In this paper, we consider a contextual dynamic pricing problem under a linear customer valuation model with an unknown market noise distribution $F$. This problem is very challenging due to the difficulty in balancing three tangled tasks of revenue-maximization, estimating the linear valuation parameter $\theta_{0}$, and learning the nonparametric $F$. To address this issue, we develop a novel {\it Explore-then-UCB} (ExUCB) strategy that includes an exploration for $\theta_{0}$-learning and a followed UCB procedure of joint revenue-maximization and $F$-learning. Under Lipschitz and 2nd-order smoothness assumptions on $F$, ExUCB is the first approach to achieve the $\tilde{O}(T^{2/3})$ regret rate. Under the Lipschitz assumption only, ExUCB matches the best existing regret of $\tilde{O}(T^{3/4})$ and is computationally more efficient. Furthermore, for regret lower bounds under the nonparametric $F$, not much work has been done beyond only assuming Lipschitz. To fill this gap, we provide the first $\tilde{\Omega}(T^{3/5})$ lower bound under Lipschitz and 2nd-order smoothness assumptions.

Video

Chat is not available.

Successful Page Load