Robust Streaming PCA

Daniel Bienstock ⋅ Minchan Jeong ⋅ Apurv Shukla ⋅ Se-Young Yun

2022 Poster

{kind=link}

Abstract

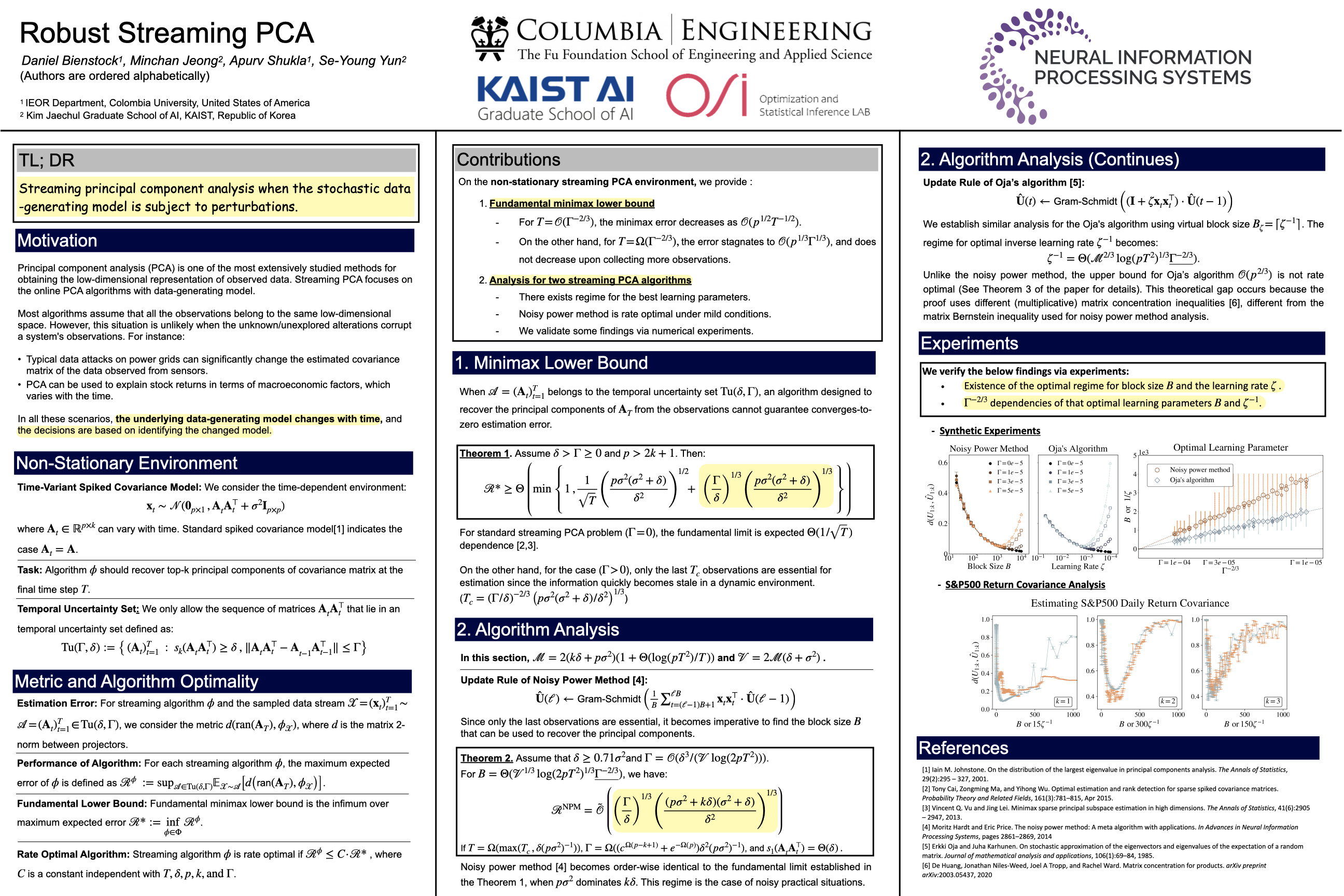

We consider streaming principal component analysis when the stochastic data-generating model is subject to perturbations. While existing models assume a fixed covariance, we adopt a robust perspective where the covariance matrix belongs to a temporal uncertainty set. Under this setting, we provide fundamental limits on any algorithm recovering principal components. We analyze the convergence of the noisy power method and Oja’s algorithm, both studied for the stationary data generating model, and argue that the noisy power method is rate-optimal in our setting. Finally, we demonstrate the validity of our analysis through numerical experiments.

Video

Chat is not available.

Successful Page Load