Regret Bounds for Risk-Sensitive Reinforcement Learning

Osbert Bastani ⋅ Jason Yecheng Ma ⋅ Estelle Shen ⋅ Wanqiao Xu

2022 Poster

{kind=link}

Abstract

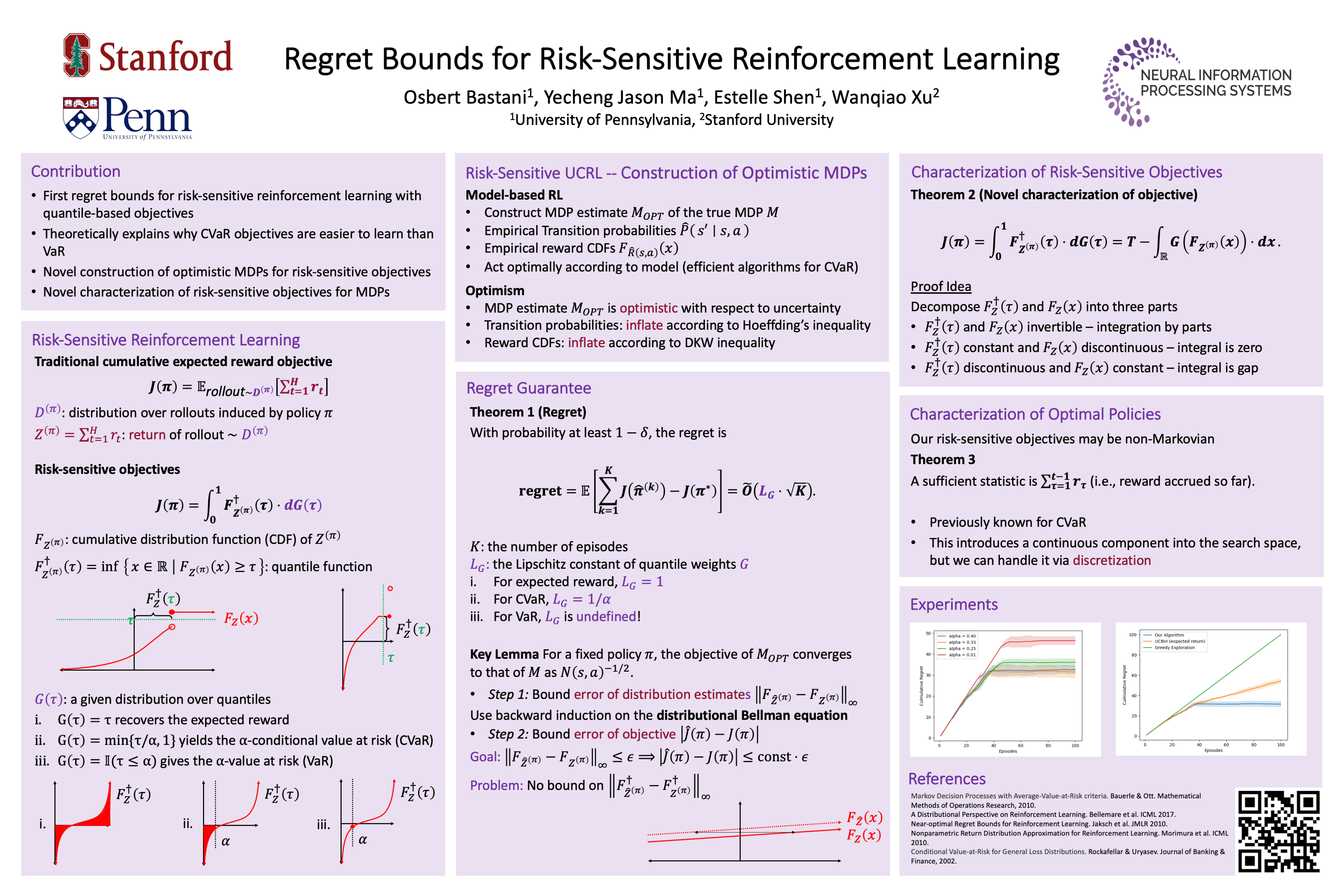

In safety-critical applications of reinforcement learning such as healthcare and robotics, it is often desirable to optimize risk-sensitive objectives that account for tail outcomes rather than expected reward. We prove the first regret bounds for reinforcement learning under a general class of risk-sensitive objectives including the popular CVaR objective. Our theory is based on a novel characterization of the CVaR objective as well as a novel optimistic MDP construction.

Video

Chat is not available.

Successful Page Load