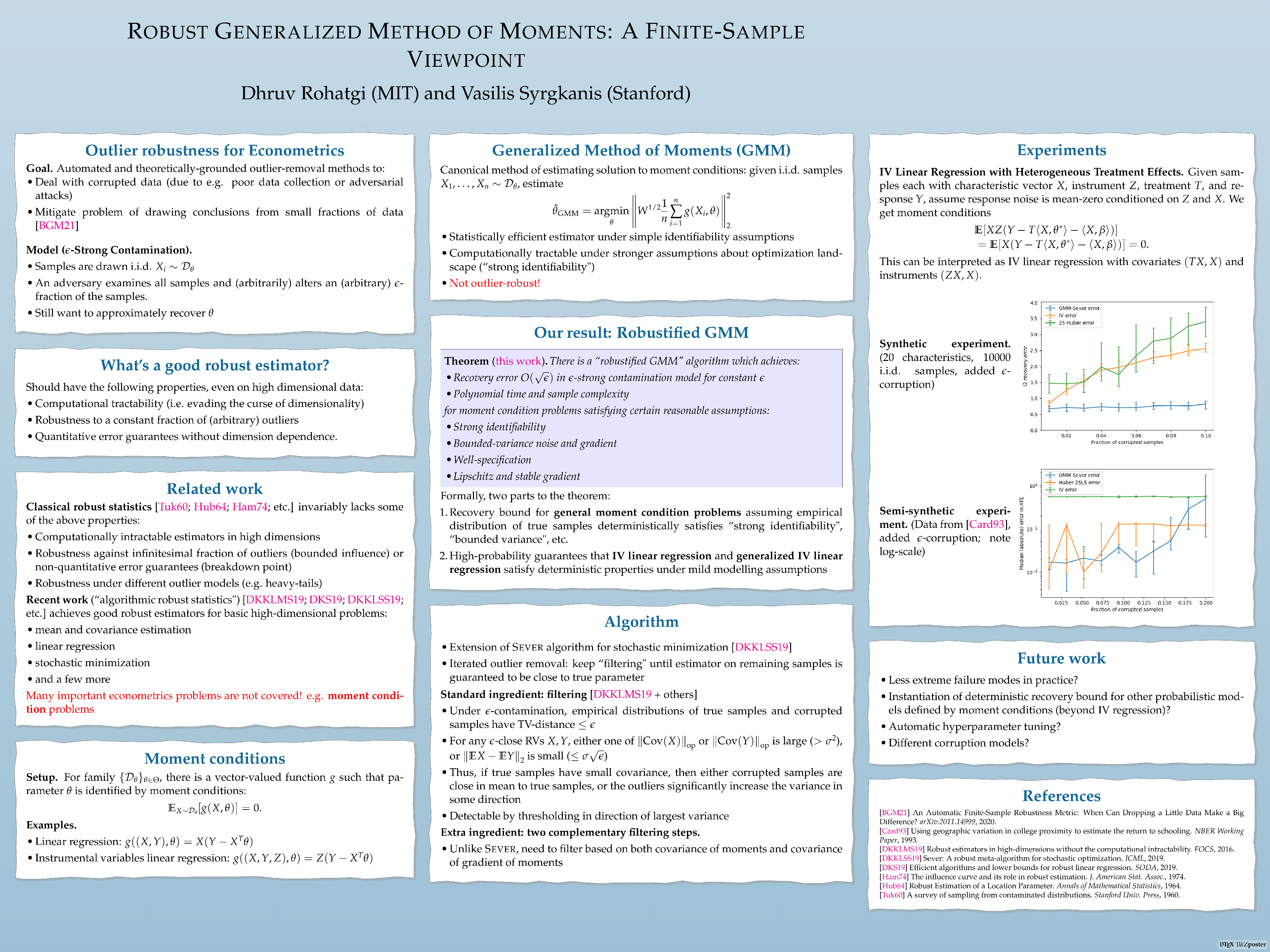

Robust Generalized Method of Moments: A Finite Sample Viewpoint

Dhruv Rohatgi ⋅ Vasilis Syrgkanis

2022 Poster

{kind=link}

Abstract

For many inference problems in statistics and econometrics, the unknown parameter is identified by a set of moment conditions. A generic method of solving moment conditions is the Generalized Method of Moments (GMM). However, classical GMM estimation is potentially very sensitive to outliers. Robustified GMM estimators have been developed in the past, but suffer from several drawbacks: computational intractability, poor dimension-dependence, and no quantitative recovery guarantees in the presence of a constant fraction of outliers. In this work, we develop the first computationally efficient GMM estimator (under intuitive assumptions) that can tolerate a constant $\epsilon$ fraction of adversarially corrupted samples, and that has an $\ell_2$ recovery guarantee of $O(\sqrt{\epsilon})$. To achieve this, we draw upon and extend a recent line of work on algorithmic robust statistics for related but simpler problems such as mean estimation, linear regression and stochastic optimization. As a special case, we apply our algorithm to instrumental variables linear regression with heterogeneous treatment effects, and experimentally demonstrate that it can tolerate as much as $10$ -- $15\%$ corruption, significantly improving upon baseline methods.

Video

Chat is not available.

Successful Page Load