Context-Based Dynamic Pricing with Partially Linear Demand Model

Jinzhi Bu ⋅ David Simchi-Levi ⋅ Chonghuan Wang

2022 Poster

{kind=link}

Abstract

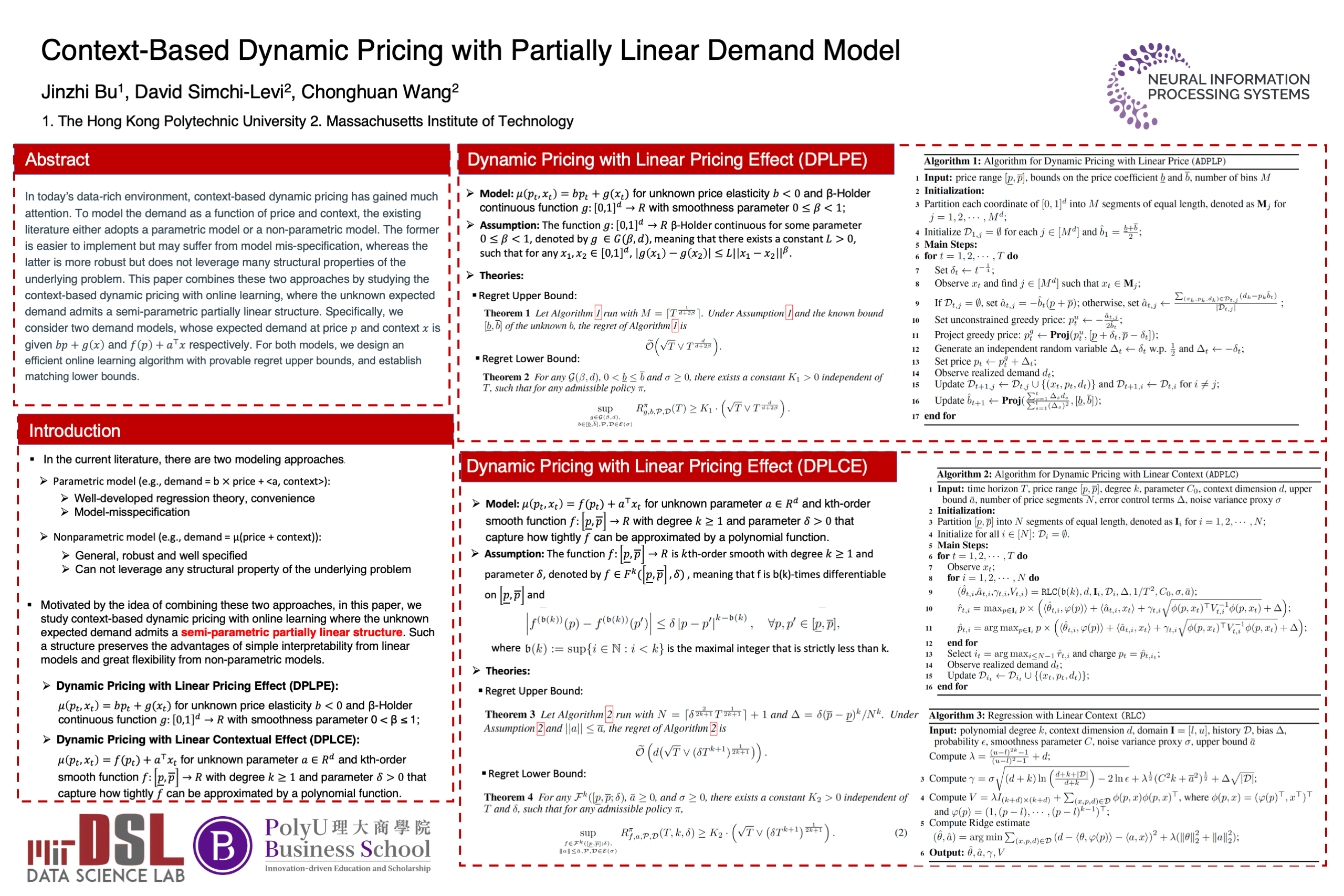

In today’s data-rich environment, context-based dynamic pricing has gained much attention. To model the demand as a function of price and context, the existing literature either adopts a parametric model or a non-parametric model. The former is easier to implement but may suffer from model mis-specification, whereas the latter is more robust but does not leverage many structural properties of the underlying problem. This paper combines these two approaches by studying the context-based dynamic pricing with online learning, where the unknown expected demand admits a semi-parametric partially linear structure. Specifically, we consider two demand models, whose expected demand at price $p$ and context $x \in \mathbb{R}^d$ is given by $bp+g(x)$ and $ f(p)+ a^\top x$ respectively. We assume that $g(x)$ is $\beta$-H{\"o}lder continuous in the first model, and $f(p)$ is $k$th-order smooth with an additional parameter $\delta$ in the second model. For both models, we design an efficient online learning algorithm with provable regret upper bounds, and establish matching lower bounds. This enables us to characterize the statistical complexity for the two learning models, whose optimal regret rates are $\widetilde \Theta(\sqrt T \vee T^{\frac{d}{d+2\beta}})$ and $\widetilde \Theta(\sqrt T \vee (\delta T^{k+1})^{\frac{1}{2k+1}})$ respectively. The numerical results demonstrate that our learning algorithms are more effective than benchmark algorithms, and also reveal the effects of parameters $d$, $\beta$ and $\delta$ on the algorithm's empirical regret, which are consistent with our theoretical findings.

Video

Chat is not available.

Successful Page Load