Learning Bipartite Graphs: Heavy Tails and Multiple Components

José Vinícius de Miranda Cardoso ⋅ Jiaxi Ying ⋅ Daniel Palomar

2022 Poster

{kind=link}

Abstract

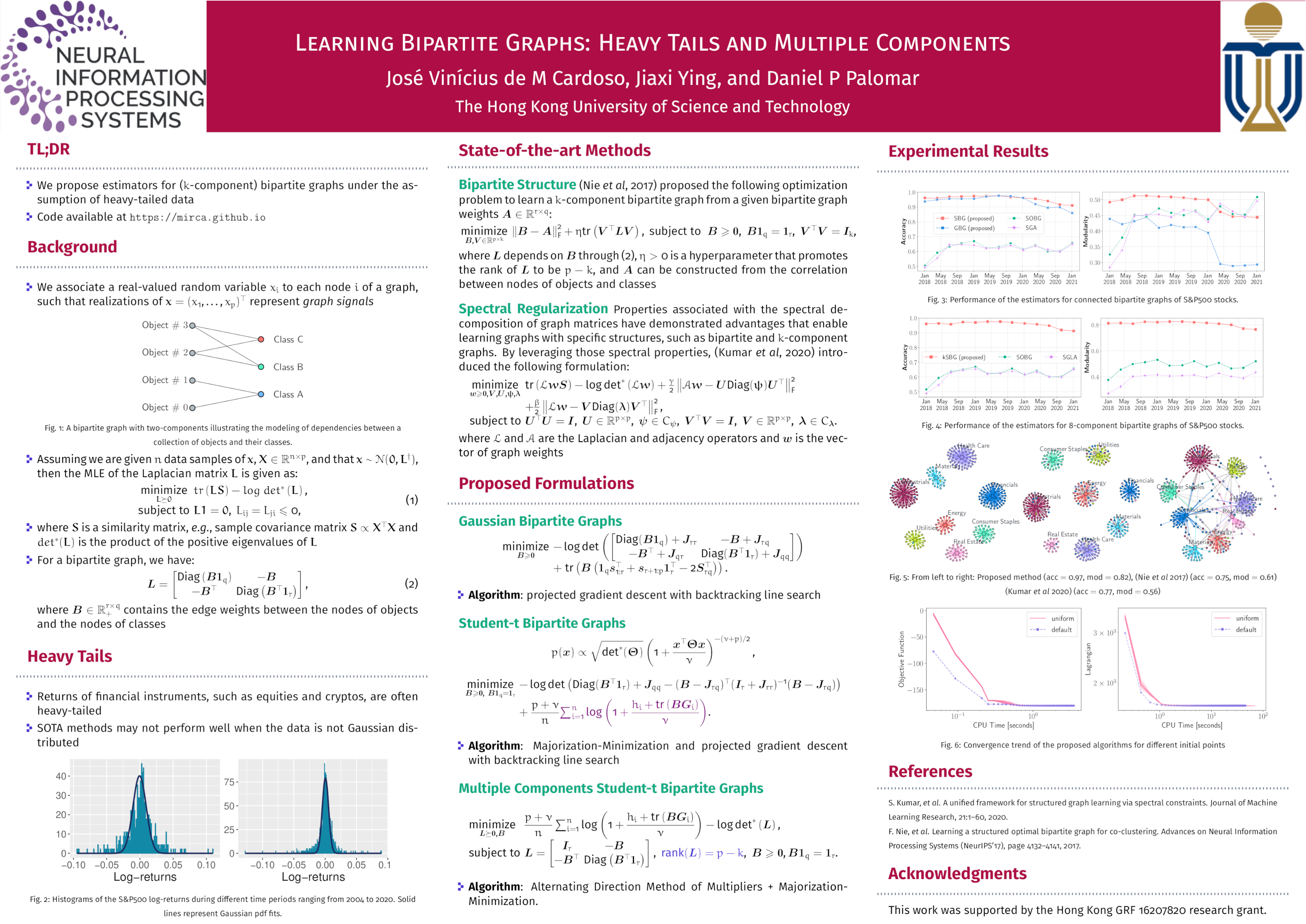

We investigate the problem of learning an undirected, weighted bipartite graph under the Gaussian Markov random field model, for which we present an optimization formulation along with an efficient algorithm based on the projected gradient descent. Motivated by practical applications, where outliers or heavy-tailed events are present, we extend the proposed learning scheme to the case in which the data follow a multivariate Student-$t$ distribution. As a result, the optimization program is no longer convex, but a verifiably convergent iterative algorithm is proposed based on the majorization-minimization framework. Finally, we propose an efficient and provably convergent algorithm for learning $k$-component bipartite graphs that leverages rank constraints of the underlying graph Laplacian matrix. The proposed estimators outperform state-of-the-art methods for bipartite graph learning, as evidenced by real-world experiments using financial time series data.

Video

Chat is not available.

Successful Page Load